Will Fossil Fuel Prices Fully Recover?

World market prices for coal have slumped and for months languished at around US$ 45/tonne, compared to US$95/tonne in February, 2014. Over the last 2 years, coal prices have more than halved and fallen almost every month.

For weeks, crude oil prices have been around US$ 30-33/barrel, sometimes falling as low as $26/barrel. Some forecasters (Goldman Sachs) predict that oil prices could stay low and do so for longer than predicted.

Some question if fossil fuel prices will ever recover given the emergence of disruptive technologies making electricity generation from renewable sources increasingly competitive with fossil fuels, even at their present depressed prices. Others point to agreement by OPEC to reduce production in order to stimulate price. However, that agreement has only been reached by 3 OPEC members (Saudi Arabia, Qatar and Venezuela) and Russia - then only when confronted by Iranian production coming on to the world market, following the lifting of international sanctions. It is seen by some as an ineffectual move to restore oil prices, since the agreement is not to exceed record high January pumping levels.

Far more certain is that the present price malaise is a taste of the state of things to come for those who have invested in the shares of fossil fuel producers. Without sustained price recovery, the value of shares in some fossil fuel companies will decline and could eventually wind-up as stranded assets of little or no value. Evidence of this is seen in closure of coal mines and the unsustainable position of oil and gas producers using older technology where cost of pumping oil and gas is close to or below its market value.

The Future of Oil

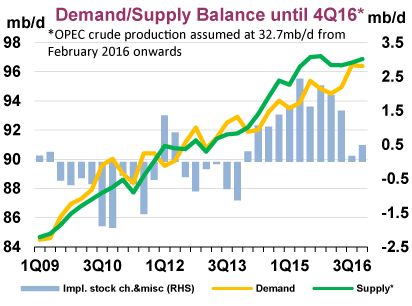

Fig 1. IEA Estimates of global supply (green) and demand (yellow) for crude oil with surplus production (Rt hand scale) held in store (blue). Estimates assume effective OPEC action to limit supply, yet be evidenced, which could see oil price recover to around $105/bbl. Source: IEA

Fig 1. IEA Estimates of global supply (green) and demand (yellow) for crude oil with surplus production (Rt hand scale) held in store (blue). Estimates assume effective OPEC action to limit supply, yet be evidenced, which could see oil price recover to around $105/bbl. Source: IEA

The present price fall for crude oil has been largely brought about by the decision of major producers to increase production to maintain income when faced with reduced demand for imported oil by China and Japan (economic slow down) and the USA (higher domestic production). The latter arises from advances in drilling and fracking technology, reducing drilling costs and vastly increasing production of gas and condensates from shale deposits and, to a lesser extent, oil.

The future for hydrocarbon producers is made more uncertain by a structural change in demand for oil products, particularly diesel and petrol. This is due to advances in battery technology, resulting in battery prices falling and increased capacity to store electricity. The result is that the range of electric cars is rapidly rising while their cost is falling. Within the next 2 years it is likely that electric cars could be selling for US$20,000 - $30,000 and have a range of 300-500 km. Competition among major car builders will ensure selling price decreases and performance improves.

Goldman Sachs analysts predict that by 2025, almost 22% of all cars in use world-wide will be propelled by electricity rather than hydrocarbons. Over the next ten years the number of electric cars is expected to increase from around 1 million to over 25 million per annum. This estimate may be conservative since it is based on improved performance criteria being achieved by 2020 (Exhibit 37) which have already been surpassed.

The result of this rapid growth in uptake of electric vehicles may well be a world-wide on-going decrease in demand for petrol and diesel. This fall in demand will be sustained and on-going. By around 2035, vehicles propelled by fossil fuels are likely to be curiosities rather than the norm, as will petrol pumps and the internal combustion engine. Thus within the next 20 years petrol and diesel will cease to be in demand for road vehicles and many off-road engines now in use.

In theory, OPEC members acting in unison, without any cheating on agreed production levels, could bring about a temporary price recovery. However, that recovery could not be sustained in the face of continuous erosion of demand for oil products due to the new economies of extracting hydrocarbons from shale and rapid adoption of electric vehicles.

The latter might be slowed by policies inimical to sale or use of electric vehicles but can not (and would not) be prevented in countries which are major consumers of road vehicles. Apart from cheaper running and operating costs, motors used in electric vehicles are over 3 times more efficient than the internal combustion engine and emit no greenhouse gases. The internal combustion engine is at best 25% efficient and a significant emitter of nitrogen oxides and particulates which are dangerous to health.

The Future of LNG

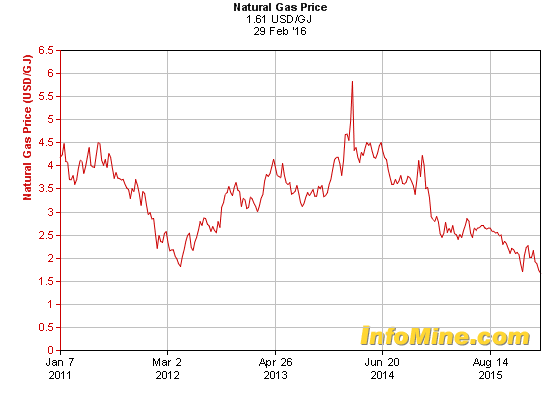

Fig. 2. LNG peak price, $5.83/GJ in 2013, arose from closure of Japan’s nuclear power stations and increasing demand from China/Europe. New technology has made USA a net exporter and China less dependent on imports, resulting in an LNG glut as new production comes on line resulting in a price collapse to $1.61/GJ.

Natural gas – largely methane – is found in coal beds, oil deposits (especially shales), other reservoirs and clathrates. Liquefied Natural Gas (LNG) is purified natural gas condensed to a liquid for ease of transport. It is widely used to meet domestic and industry energy needs and to a lesser extent for transport. LNG is largely produced from shale and sandstone deposits which are widely distributed around the world.

New technology enabling horizontal drilling and fracturing (fracking) has vastly increased gas production in countries with large shale deposits, notably Canada, USA, Australia and many others

The USA, once a major LNG importer, is now largely self-sufficient and is presently a net exporter. Japan, another major importer, has begun selling surplus LNG stock as it re-opens its nuclear power plants, adding to the LNG glut in the short-term. Into this glut 4 major Australian LNG projects (costing $118 billion) will come on line in 2016-17, mitigating against medium term LNG price recovery, lowering target return on investment and reducing its contribution to public revenue.

Demand for product has fallen at the same time as capacity to produce has increased. The result has been a dramatic collapse in the price of LNG.

This collapse could result in more extensive use of LNG and increase demand resulting in price recovery. This may occur in the longer-term but over the next 10 years this seems unlikely because existing and emerging suppliers (Iran) are likely to adopt new drilling technology, as China is doing, increasing self-sufficiency and prolonging present global LNG over-production.

LNG must compete with other energy forms, notably solar energy which over the coming decade is likely to become price competitive, reducing the need for LNG imports and expensive cryogenic storage and infrastructure. Burning LNG produces CO2 and commitments made under the Paris Agreement may discourage its use where competitive renewable energy is available. The prospect for longer term LNG price recovery to levels seen in 2013 seems unlikely.

If the LNG industry were confident of its longer-term future, it would now be investing in costly processing and storage facilities but this is not the case. Deferral or cancellation of major investment in new LNG processing plants in Canada, the USA and Norway have occurred recently.

The Future of Coal

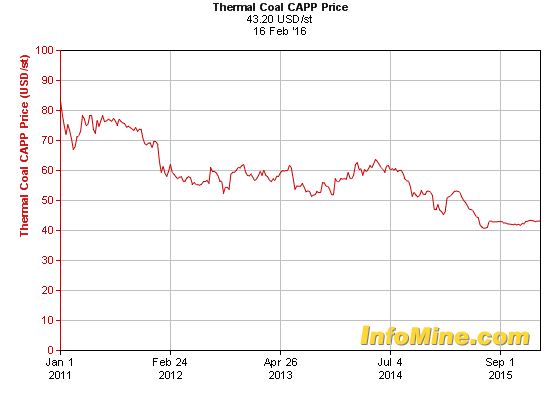

Fig 3. World price for thermal coal has fallen below $50/tonne since July 2015 forcing Anglo-American, Glencore and others to close small to medium coal mines. Only larger mines continue to operate profitably.

Fig 3. World price for thermal coal has fallen below $50/tonne since July 2015 forcing Anglo-American, Glencore and others to close small to medium coal mines. Only larger mines continue to operate profitably.

Prima facie, transition towards wide use of electric motors in road vehicles should mean a rapid increase in demand for electricity since the batteries of electric vehicles must be repeatedly re-charged. This should result in greater demand for coal from power stations, forcing a rise in price from the present low of $43/tonne – a price so low that smaller to medium sized coal mines have difficulty operating profitably.

This would be the case were it not for development of batteries able to propel vehicles over 1,000 km on a single charge. Those same batteries are now becoming available for storing electricity generated from photovoltaic cells (PVC’s) mounted on house roof-tops and a growing number of solar power stations. This enables dwellings to use auto-generated electricity after sunset and PVC solar power stations to supply electricity 24/7.

In 2015, the Tesla gigafactory was the largest producer of batteries for domestic and commercial electricity storage. However factories in Korea, China and Spain are now well established offereing competition in technology advances, battery characteristics and price. In 2016 this is resulting in consumers having a range of batteries and prices to choose from and enabling domestic dwellings to store and trade surplus electricity generated by PVC’s on their roofs.

In Australia, over 1,250,000 houses have PVC displays with capacity to generate 5 GW or 9% of Australia’s total electricity generation capacity. Many households will purchase batteries and sell electricity to the grid, to energy providers or to each other for domestic use, including recharging electric vehicle batteries. This will result in reduced demand for electricity generated by coal fired power stations, reducing demand for coal.

Demand for coal to generate electricity and for metal smelting will further reduce as solar powered utilities, using increasingly efficient technology, continue to be established – a process well underway in North America, Europe and North East Asia. Use of coal could be further reduced with reform of building regulations to mandate installation of PVC arrays and solar hot water systems on new dwellings and increased oil production as new mining technology becomes more widely used.

Inability of coal prices to recover is exacerbated by emerging disruptive technologies which have already resulted in doubling the efficiency with which PVC’s convert sunlight into electricity. The latter are likely to become commercially available before 2020, further reducing cost of solar generation and increasing surplus electricity available for recharging electric vehicle batteries. Battery technology is also making advances, particularly through use of Graphene in cathodes and PVC’s. This promises to significantly increase solar generation, storage capacity and durability, while reducing cost of storing energy.

These developments, the more efficient use of electricity and the Paris Agreement on reduction of greenhouse gasses increase the speed of transition from coal to solar generated electricity and mitigate against longer term price recovery for coal. In the short term some price recovery may occur but is likely to be short lived as use of solar energy increases.

Conslusion

Coal use for electricity generation is becoming uncompetitive with solar energy because new technologies make solar electricity generation and storage increasingly cost-efficient. Coal is in the invidious position of having to compete against a free product – solar energy.

Due to adoption of new technologies, the world is currently awash with hydrocarbons, making their price so low that the cost of finance needed for new exploration has become difficult to obtain. OPEC Members have agreed not to exceed present production levels but not to reduce them.

This mitigates against sustained recovery of fossil fuel prices in the short-term. In the medium term, demand for fossil fuels, particularly oil and LNG, are unlikely to increase because advances in battery technology make it possible to store solar generated electricity, ensuring 24/7 availability and increasing the rate of electric vehicle uptake.

The transition to electric vehicles and greater use and demand for non emitting solar power generation indicate on going decline in demand and price of all fossil fuels in the longer term.

This tends to substantiate warnings in the finance industry that existing investments in the fossil fuel industry could become stranded assets with the cost of future investment rising as predicted demand for fossil fuels becomes less certain.

Will fossil fuel prices fully recover? In the short term, its possible but recovery is unlikely to be sustained. In the longer term, price recovery is much less likely.

Posted by Riduna on Friday, 4 March, 2016